If you are self-employed, tax season can feel like a one-way road where your money goes out far more than it comes back in.

Unlike W-2 employees, whose employers cover half of their Social Security and Medicare taxes, you are accountable for the full 15.3% self-employment tax on your income. That’s where the Self Employment Tax Credit becomes relevant.

You might often see it mentioned online, but you won’t find a clear explanation, especially when it comes to claiming it retroactively. At Skyline Financial Management, we have seen how easy it is to miss this credit entirely or claim it incorrectly. As we move through 2026, the window to claim it is narrowing, and the margin for error is smaller than ever.

This guide walks you through how the credit works and how you can claim it in easy steps.

A Simple Explanation of the Self Employment Tax Credit

The Self-Employment Tax Credit (SETC) is a refundable tax credit that was introduced under the Families First Coronavirus Response Act (FFCRA). It was created to give self-employed individuals access to the same paid sick and family leave benefits that employees received during the COVID-19 pandemic.

If you were unable to work because you were sick, quarantined, or caring for a child whose school or daycare was closed, the IRS allows you to claim a “daily rate” for those missed workdays. Because this credit is refundable, it can reduce your tax bill and still result in a refund if the credit is more than what you owe.

Who Can Still Claim the Credit in 2026?

Since the credit applies to 2020 and 2021, you will usually need to file an amended return to claim it today.

You may qualify if:

- You were self-employed in 2020 or 2021.

- You reported net profit on Schedule C.

- You missed work during specific COVID-related periods.

There are two primary eligibility windows:

- April 1, 2020, to March 31, 2021.

- April 1, 2021, to September 30, 2021.

It’s important to note that you must have had net self-employment income. If your Schedule C showed a loss, you can’t claim the credit for that year.

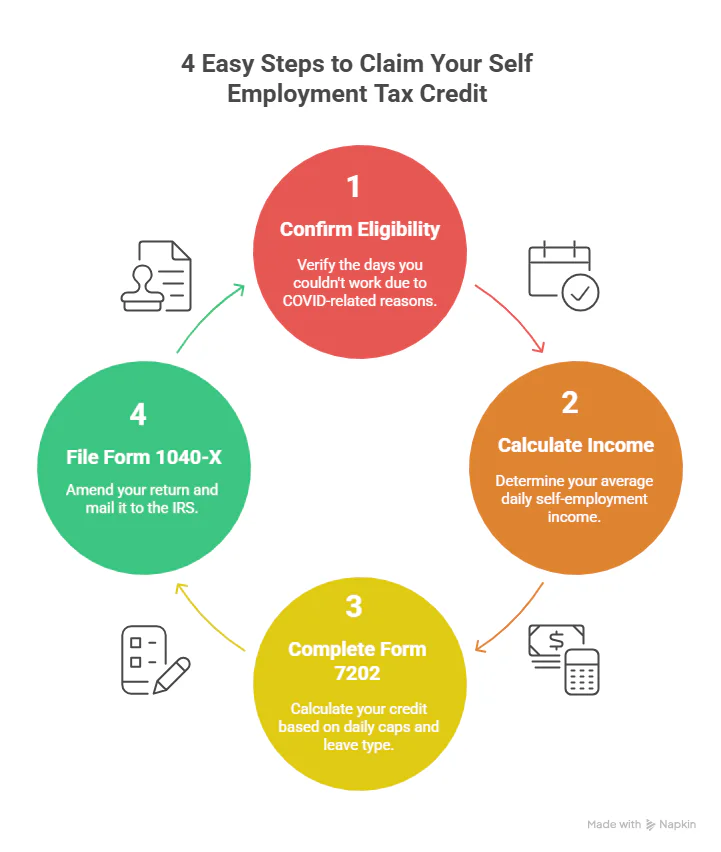

4 Easy Steps to Claim Your Self Employment Tax Credit

Step 1: Confirm Your Eligibility Window

You need to figure out the specific days you were not able to work due to COVID-related reasons. The IRS is strict about dates, so you must be accurate with them.

Overstating days is one of the fastest ways to invalidate your claim.

Step 2: Calculate Your Average Daily Income

Your credit depends on your average daily self-employment income:

Here’s how it works:

- Take your net earnings from self-employment (Schedule SE).

- Divide that number by 260.

For example, if your net earnings were $65,000, your average daily income is $250.

Step 3: Complete IRS Form 7202

Form 7202 is where your credit is calculated. It separates:

You will enter:

- The number of days you couldn’t work.

- Whether the leave was for your own illness or family care.

Daily caps apply:

- Up to $511 per day for your own illness.

- Up to $200 per day for caregiving or school closures.

This step directly affects your self-employment tax preparation, so precision is very important here.

Step 4: File Form 1040-X

Because original filing deadlines have passed, you must amend your return using Form 1040-X to claim your credit. You will attach Form 7202 and mail the amended return to the IRS. There is no e-file option for this process.

The Missing Elements That Can Cause the IRS to Reject Your Filing

This is where many online guides fall short.

1. The PPP Overlap Problem

If you acquired a Paycheck Protection Program (PPP) loan, you cannot claim the SETC for the same days covered by PPP owner compensation replacement.

This overlapping issue is the most common reason the IRS disallows credits and demands repayment with interest.

2. The Documentation Gap

You don’t submit proof with your return, but you must keep it.

Acceptable records include:

- Positive COVID test results.

- Doctor’s notes.

- School or daycare closure notices.

If you are audited years later, the lack of documentation can result in penalties even if your calculation was correct.

3. The 2019 Look-Back Election

If your income dropped in 2020, you may be allowed to use 2019 earnings to calculate your daily rate.

This can significantly increase your refund, but most tax software automatically focuses on the current year and never flags this option for you.

4. Sick Leave vs. Family Leave

There are two different parts of the credit:

- Sick leave: Up to 10 days at 100%.

- Family leave: Up to 50 to 60 days at 67%.

Many filers only claim sick leave and miss the much larger family leave credit. If you stayed home due to childcare disruptions, this portion may apply even if you were never ill.

If you’re self-employed or running a startup and feel overwhelmed by self-employment taxes or claiming credits correctly, our Online CPA services for startup and self-employed business owners can guide you step-by-step.

Self Employment Tax Credit FAQs

1. Is the Self Employment Tax Credit still available in 2026?

It’s possible, but only through amended returns, and the deadlines are tight.

2. Do I need proof to claim it?

You don’t submit proof, but you must keep it in case of an audit.

3. What if I worked part-time during COVID?

You may still qualify for days you were unable to work due to qualifying reasons.

4. Is the credit taxable income?

The credit itself is not taxable, but it reduces the deductible portion of your self-employment tax.

5. What happens if I claim it incorrectly?

The IRS may disallow your credit, assess penalties, and charge interest.

Conclusion

The Self Employment Tax Credit was created to help people like you, but claiming it correctly takes more than just a calculator and a form.

At Skyline Financial Management, we take a conservative and documentation-first approach. If you are unsure whether you qualify or want to review an amended filing before you submit it, now is the time to connect with our certified Houston CPA, Zahra Samji.

Schedule a consultation today before the window closes, so you don’t miss this valuable opportunity!