Health insurance is among the biggest expenses you carry as a self-employed individual, and it is also one of the most valuable deductions available on your tax return if you claim it correctly.

The self-employed health insurance deduction lets you claim 100% of premiums paid for health, dental, and vision coverage for yourself, your spouse, and your dependents directly from your gross income. Unlike most medical expense deductions that are subject to adjusted gross income thresholds and itemization requirements, this one comes off the top of your income as an above-the-line deduction.

That distinction makes it powerful, but it also comes with eligibility rules, income limitations, and interaction effects that are worth understanding before you assume you qualify and how much you can claim.

The Eligibility Rules That Determine Whether You Can Actually Claim This Deduction

Not every self-employed person qualifies for the self-employed health insurance deduction every year, and the conditions that disqualify you are specific enough that they often create confusion during return preparation.

The fundamental requirement is that you must have a net profit from self-employment. The deduction is strictly limited to your net profit from the business under which the insurance plan was established.

If your business operated at a loss for the year, you cannot claim the deduction, though you may still be able to deduct premiums as an itemized healthcare expense, subject to the standard AGI floor.

The eligibility conditions that matter most are:

- You must be self-employed as a sole proprietor, partner in a partnership, member of an LLC taxed as a partnership, or a more-than-2% shareholder in an S-corporation.

- The health insurance plan must be established under your business.

- You cannot be eligible for coverage through an employer-sponsored health plan through your own or your spouse’s employment.

- The deduction cannot be higher than your net profit from the self-employment activity.

That last condition is the one that most frequently creates problems. If your spouse has access to employer-sponsored coverage that you are eligible to enroll in, you can’t claim the self-employed health insurance deduction for any month that coverage was available to you, even if you chose not to enroll.

How S-Corporation Shareholders Claim This Deduction Differently

The mechanics of this deduction work differently depending on your business structure, and S-Corporation treatment is where errors are most common.

If you are a more-than-2% shareholder in an S-corporation, the health insurance premiums the corporation covers on your behalf must be included in your W-2 wages as compensation. The corporation can deduct the premiums as a compensation expense, and you then claim the deduction on your personal return to offset that income.

The critical requirement is that the premiums must appear in Box 1 of your W-2. If the corporation pays the premiums but does not include them in your reported wages, the IRS treats the arrangement as improperly structured, and you lose the deduction.

For sole proprietors and single-member LLC owners, the process is more straightforward. You pay the premiums directly, report them on Schedule 1 of Form 1040, and the deduction reduces your adjusted gross income without needing to flow through payroll.

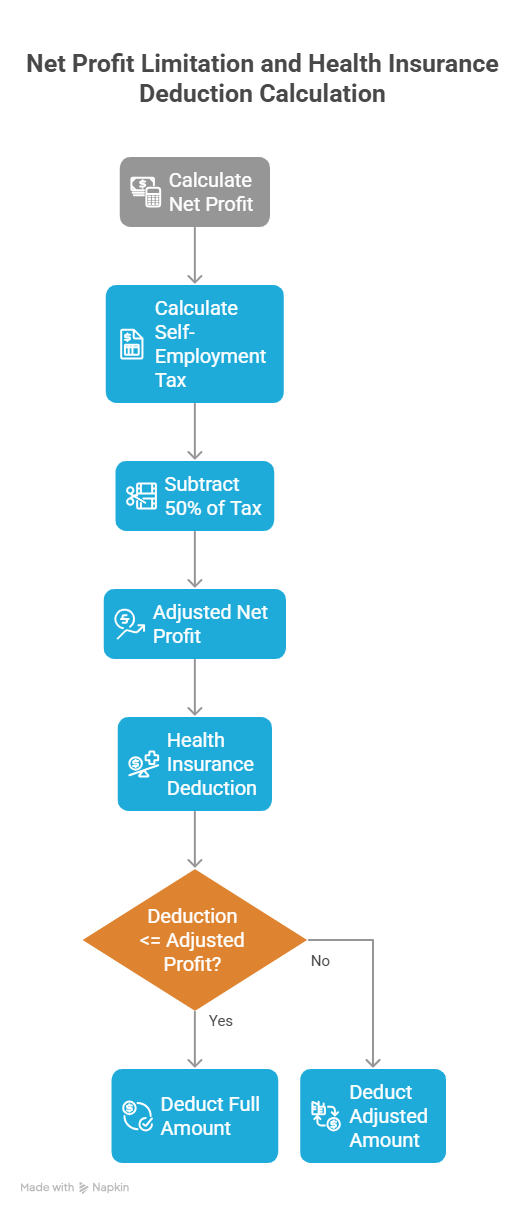

The Net Profit Limitation and Its Interaction with Self-Employment Tax

Your self-employed health insurance deduction is limited to your net profit from self-employment, but that net profit is calculated after subtracting the deductible portion of self-employment tax, which is 50% of your total liability.

The calculation follows this sequence:

- Calculate your net profit from Schedule C or partnership income.

- Calculate your self-employment tax.

- Subtract 50% of that tax from your net profit.

- Your health insurance deduction cannot exceed that adjusted figure.

This interaction requires sequential calculation rather than independent treatment. Overestimating your deduction by ignoring this adjustment is a common error that creates discrepancies with IRS expectations.

What Qualifies as a Deductible Premium

Not every health-related expense qualifies under the self-employed health insurance deduction, and the distinction affects how you categorize expenses.

- Medical, dental, and vision insurance premiums qualify.

- Long-term care insurance premiums qualify, subject to age-based limits.

- Medicare Part B and Part D premiums qualify if you are self-employed.

- Out-of-pocket medical expenses do not qualify and fall under Schedule A.

- Supplemental insurance generally does not qualify.

Long-term care insurance premiums deserve attention because the qualifying amount changes annually based on age.

If you pay more than the allowable limit, the excess does not qualify for the above-the-line deduction but may still be deductible as an itemized expense.

Key Takeaway

The self-employed health insurance deduction is considered one of the most valuable above-the-line deductions available to you, but it requires accurate eligibility analysis, correct handling based on your entity type, proper interaction with your self-employment tax calculation, and coordination with marketplace credits.

Getting these elements right is what separates a return that fully reflects your deductions from one that leaves money on the table or creates compliance risk.

At Skyline Financial CPA in Houston, you work directly with Zahra Samji, who ensures your deduction is structured correctly and your return reflects every legitimate benefit available to you.

If you are ready to stop taking chances and start filing with confidence, booking a consultation with her gives you the clarity your tax situation deserves.

FAQs

Can I claim the deduction if my business had a loss this year?

No. The deduction is limited only to your net profit, so if your business operated at a loss, you cannot claim it. You may still deduct premiums as an itemized expense subject to the AGI floor.

Does the deduction reduce self-employment tax?

No. It reduces your adjusted gross income for income tax purposes but does not reduce the net profit used to calculate self-employment tax.

Can I deduct premiums for my spouse and children?

Yes. The deduction covers premiums for you, your spouse, dependents, and children under age 27, even if they are not claimed as dependents.

What if I were eligible for employer coverage through my spouse?

You cannot claim the deduction for any month you were eligible for employer-sponsored coverage, even if you did not enroll.

Are Medicare premiums deductible?

Yes. Medicare Part B, C, and D premiums qualify if you meet the other eligibility requirements and are not eligible for employer-sponsored coverage.