Running a manufacturing operation means managing financial complexity that most other business types never encounter.

Your costs are layered across raw materials, direct labor, machine time, and overhead allocations that shift with every production run. Your inventory exists in multiple states simultaneously, as raw materials and finished goods, each carrying a different valuation. And your profitability on any given product line depends entirely on whether your cost accounting reflects what is actually happening on the floor.

Goal-specific manufacturing accounting services give your factory the financial infrastructure to track those costs accurately, report performance honestly, and make decisions based on numbers that reflect operational reality rather than accounting assumptions.

Why Standard Cost Accounting Creates a False Picture of Your Production Profitability

Most manufacturers are familiar with standard costing, but few understand how quickly standard costs can drift from actual costs and what that drift does to your decision-making.

Standard costing assigns predetermined costs to materials, labor, and overhead. The gap between those costs and actual production costs is called a variance. Variance analysis is where real financial intelligence lives.

If your current accounting setup records variances but nobody analyzes them systematically, you are missing actionable insights that could improve margins.

The key variances to track include:

- Material price variance: Difference between expected and actual raw material costs.

- Material usage variance: Difference between standard and actual material consumption.

- Labor rate variance: Difference between the standard labor cost per hour and the actual pay.

- Labor efficiency variance: Difference between standard hours allowed and actual hours worked.

- Overhead volume variance: Difference between budgeted and absorbed fixed overhead.

When your accounting services Houston consistently produce and analyze these variances, you can manage your factory with real data, not averages, and address inefficiencies before they compound.

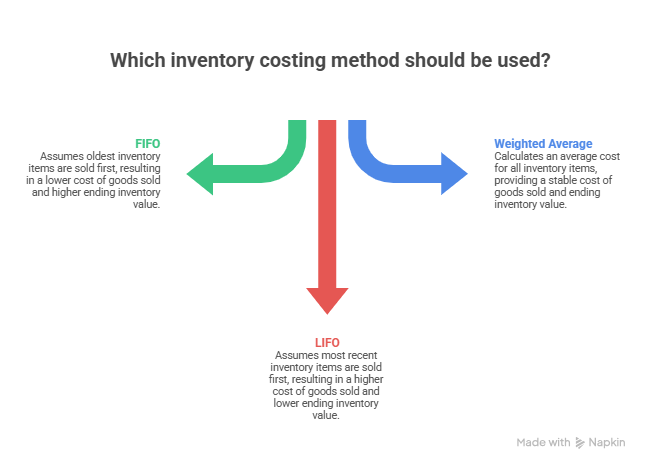

Inventory Costing Methods and Why Choosing the Wrong One Affects Both Your Tax Bill and Your Margins

Your inventory costing method affects your cost of goods sold and your balance sheet. In periods of rising material costs, the method you choose can change reported profitability and taxable income.

| Method | How COGS Is Calculated | Inventory Value | Tax Impact |

| FIFO | Oldest costs first | Reflects recent higher costs | Higher taxable income |

| LIFO | Latest costs first | Reflects older, lower costs | Lower taxable income |

| Weighted Average | Average of all costs | Smoothed across units | Moderate taxable income |

LIFO is only allowed under US GAAP, not IFRS. Once chosen for tax purposes, switching requires IRS approval and may trigger recapture of prior reserves.

Choosing the right method is a decision best made with professional manufacturing accounting services to avoid costly mistakes.

How Overhead Allocation Errors Silently Distort Your Product Line Profitability

Overhead allocation is often overlooked but directly affects perceived product profitability. Traditional plantwide rates distribute costs evenly across products, which can misrepresent margins when products consume overhead differently.

Activity-Based Costing (ABC) allocates overhead based on the activities driving costs, such as machine setups, inspections, material handling, and production runs. A low-volume specialty product requiring multiple setups will have costs reflected accurately, unlike with plantwide allocation.

Dedicated manufacturing accounting services at Skyline Financial CPA ensure overhead is allocated based on actual activity, giving you the clarity to price and produce efficiently.

Tax Considerations in Manufacturing That Go Beyond the Standard Business Return

Manufacturing businesses have access to tax provisions that are specifically designed for the industry, and they are among the most valuable in the tax code for businesses that qualify.

Understanding them is a meaningful part of what well-structured manufacturing accounting services deliver.

The Section 199A Qualified Business Income Deduction

It allows eligible pass-through manufacturers to deduct up to 20% of qualified business income, subject to W-2 wage limitations that make payroll structure a direct input into the deduction calculation.

If your factory operates as an S-corporation or partnership, the way you manage compensation and distributions affects how much of this deduction you can claim.

Research and Development Tax Credits under Section 41

It applies to manufacturers who engage in process improvement, product development, or engineering activities that involve experimentation.

Many manufacturers do not claim these credits because they associate R&D with laboratory research, but qualifying activities include developing new manufacturing processes, improving existing processes, and testing new materials for use in production.

Section 179 and Bonus Depreciation

This applies to manufacturing equipment, allowing you to expense significant capital purchases in the year of acquisition rather than depreciating them over the asset’s useful life.

For a manufacturer investing in new equipment, coordinating these elections with your quarterly estimated tax payments can dramatically reduce your year-end tax liability.

Final Reflection

Manufacturing accounting is not a variation of standard business bookkeeping. It is a specialized discipline that requires cost accounting structures, inventory valuation methodology, overhead allocation design, and tax planning strategies that generic financial management simply cannot provide.

When your books are built around how your factory actually operates, your financial data becomes a management tool rather than a compliance exercise.

At Skyline Financial, we work directly with manufacturing business owners who need accounting that reflects the real economics of their operation. Zahra brings the licensed Houston CPA expertise to structure your cost accounting, evaluate your inventory methodology, and ensure your tax position captures every provision your business qualifies for.

Reach out now and schedule a consultation with Houston manufacturing CPA firm to put professional manufacturing accounting expertise behind your operation.

Manufacturing Accounting Services FAQs

What do manufacturing accounting services include that standard accounting does not?

They include job costing or process costing, variance analysis, inventory valuation methods, overhead allocation, and Work in Progress tracking. These are the functions that standard accounting setups cannot handle accurately.

How does variance analysis help improve profitability?

It compares standard costs to actual costs, pinpointing where production is costing more than planned and highlighting processes, suppliers, or labor patterns that need adjustment.

What is the difference between job costing and process costing?

Job costing tracks costs by individual production order, ideal for custom batches. Process costing tracks costs by production process, suited for continuous or homogeneous output.

Can manufacturers claim the R&D tax credit without a dedicated research department?

Yes. Section 41 credits apply to qualifying activities involving experimentation or process improvement, even if conducted on the production floor.

How do manufacturing accounting services support better pricing decisions?

They give you an accurate cost per unit reflecting actual material, labor, and overhead, enabling confident pricing and evaluation of product profitability before committing to changes.