You face financial realities in construction that most other industries don’t. Your revenue comes in draws and progress billings, your costs shift with material prices and subcontractor schedules, and profit on any project isn’t confirmed until the job closes.

Generic bookkeeping wasn’t built for this. Construction accounting services are designed to match how your business actually operates, from income recognition to job-level cost tracking.

Without this focus, your books won’t give you a true picture of where your business stands.

Why Percentage of Completion Accounting Changes Everything for Contractors

Most service businesses recognize revenue when payment is received or a service is completed. Your projects don’t work that way, and using the wrong revenue recognition method can misrepresent your financial position.

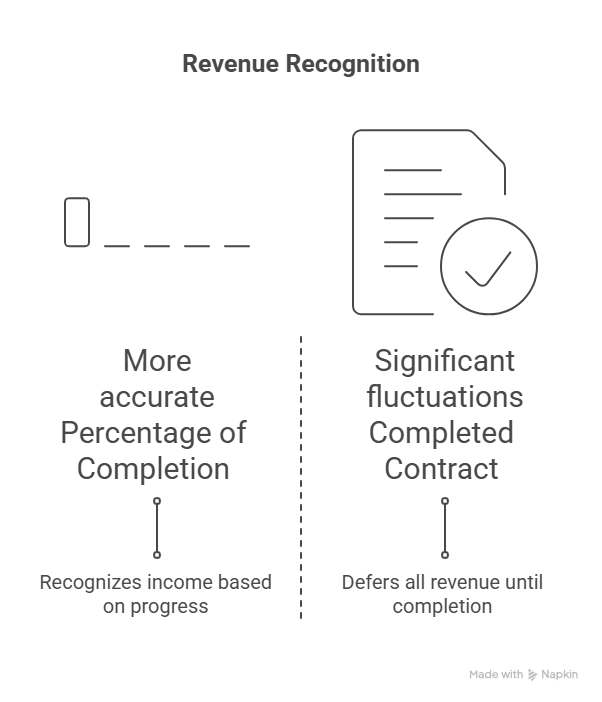

The two main methods are:

Percentage of Completion (POC)

You recognize revenue and expenses in proportion to project completion, usually measured by costs incurred versus total estimated costs. This gives you an accurate view of profitability across reporting periods, matching income to the work actually done.

Completed Contract Method

You defer revenue and expenses until a project is substantially complete. While simpler, it can distort your financial statements when multiple long-term projects are active.

For projects spanning multiple accounting periods, a POC is usually required under GAAP. It gives lenders, bonding companies, and project owners a clear view of your financial health. Getting it right isn’t optional because it affects your ability to secure bonding and financing.

Job Costing Is the Engine of Your Profitable Construction Business

Job costing is what separates construction accounting from generic small business bookkeeping. Every project should have its own cost structure, tracking labor, materials, subcontractors, equipment, and overhead.

Without it, your profit and loss statement only shows overall profitability. With it, you can see which projects succeed, which underperform, and where variances occur.

A good job costing system tracks:

- Direct labor by employee and trade, tied to specific project codes.

- Material purchases are allocated to jobs at purchase.

- Subcontractor costs are invoiced to specific projects and phases.

- Equipment costs by actual usage hours.

- Overhead is distributed fairly using a predetermined rate.

With construction accounting services focused on job costing, you can run a cost report on any project and know exactly how you compare to your estimates. This visibility lets you catch overruns before they become costly surprises.

Work in Progress Reports and Why Bonding Companies Scrutinize Them

If you pursue bonded work or public contracts, your Work in Progress (WIP) schedule is one of the most important financial documents you produce. Bonding companies use it to assess whether your business can complete contracted work, and errors can affect your bonding capacity.

A WIP report summarizes every active project’s status:

| Column | What It Represents |

| Contract Value | Total agreed contract amount |

| Costs Incurred to Date | Actual costs posted to the job |

| Estimated Cost at Completion | Original or revised total cost estimate |

| Percent Complete | Costs incurred ÷ estimated total costs |

| Earned Revenue | Contract value × percent complete |

| Billed to Date | Total amounts invoiced |

| Over/Underbilling | Earned revenue − billed amounts |

Bonding companies focus on over/underbilling. Underbilling can indicate cash flow issues, while overbilling may suggest work isn’t keeping pace with invoicing.

Accurate construction accounting services at Skyline Financial CPA ensure your WIP schedule reflects reality and strengthens your bonding relationships.

Payroll Compliance Risks That Affect You

Construction payroll is more complex than most industries, and mistakes carry risk. For public projects, prevailing wage rules under the Davis-Bacon Act require you to pay locally determined wages for each trade. Misclassifying workers or underpaying can create serious liability.

Other compliance obligations include:

- Correct classification of employees vs. independent subcontractors.

- Certified payroll reporting for federally funded projects.

- Workers’ compensation calculations by classification code.

- Union labor reporting obligations.

Your accounting system should support these requirements, not just generate paychecks. When payroll and job costing are integrated, labor costs flow directly into project reports, giving you real-time insight into labor burdens by project.

Tax Considerations That Are Unique to Your Business

Construction businesses have access to tax strategies that standard bookkeeping doesn’t cover.

The look-back method adjusts prior-year tax liability for long-term contracts using POC, correcting differences between estimated and actual costs. This can result in interest charges or credits.

Section 460 defines which contracts must use POC for tax purposes. Small contractors under the gross receipts exemption may use the completed contract method for tax reporting while still using POC for financial reporting, creating a timing difference.

Owning construction equipment gives you access to Section 179 expensing and bonus depreciation, reducing taxable income in high-revenue years. Coordinating these deductions with your quarterly estimated taxes is a planning opportunity that specialized construction accounting can help you navigate.

Concluding Remarks

Construction accounting isn’t just small business bookkeeping. It requires job costing, WIP reporting, revenue recognition, and payroll compliance.

With purpose-built construction accounting services, your books give you clear insight into project performance, protect bonding capacity, ensure compliance, and support proactive tax decisions.

At Skyline Financial CPA in Houston, we work directly with contractors like you who need financial clarity that matches your work’s complexity. Zahra Samji structures her accounting services Houston around your operations so your numbers provide answers, not questions.

Get in touch with Houston construction accounting firm today to build a financial foundation that supports your business at every stage.

Construction Accounting Services FAQs

How does job costing improve profitability?

Job costing assigns all labor, materials, subcontractor, and overhead costs to projects. This lets you compare costs to estimates, spot overruns early, identify profitable projects, and improve future bids.

What is a WIP schedule, and why do bonding companies require it?

A WIP schedule summarizes active projects’ financial status, including contract value, costs, estimated completion, earned revenue, and over/underbilling. Bonding companies use it to assess financial capacity, and errors can limit bonding.

How do prevailing wage requirements affect payroll accounting?

Prevailing wage sets minimum pay by trade classification for federally funded projects. Payroll must track classifications, confirm correct rates, and produce certified reports. Non-compliance carries back pay and contract risks.

Can construction businesses use the completed contract method for tax purposes?

Small contractors meeting Section 460 gross receipts exemptions may use the completed contract method for tax reporting, even if using POC for financial reporting. Proper construction accounting services help manage this deferral based on revenue, project length, and overall tax position.