Building a business is rewarding, but without structured startup tax services, you may pay more in taxes than necessary during your earliest growth phase. Many founders focus on revenue generation and product development, only to realize later that poor tax planning reduced cash flow and created compliance stress.

The right tax strategy from the beginning allows you to preserve capital, claim eligible deductions, and avoid preventable penalties.

At Skyline Financial CPA Houston, we help you approach taxes proactively so the decisions you make today do not create financial strain tomorrow.

Why Early Tax Strategy Shapes Long-Term Profitability

Your startup’s first few years impact long-term financial health. Early mistakes such as improper entity selection, missed elections, or overlooked deductions can compound over time.

Without proper planning, you may face:

- Overpayment of self-employment taxes.

- Missed startup expense deductions.

- Incorrect estimated tax payments.

- State compliance penalties.

- Poor recordkeeping that complicates audits.

Effective startup tax services focus on structuring your business correctly before problems arise.

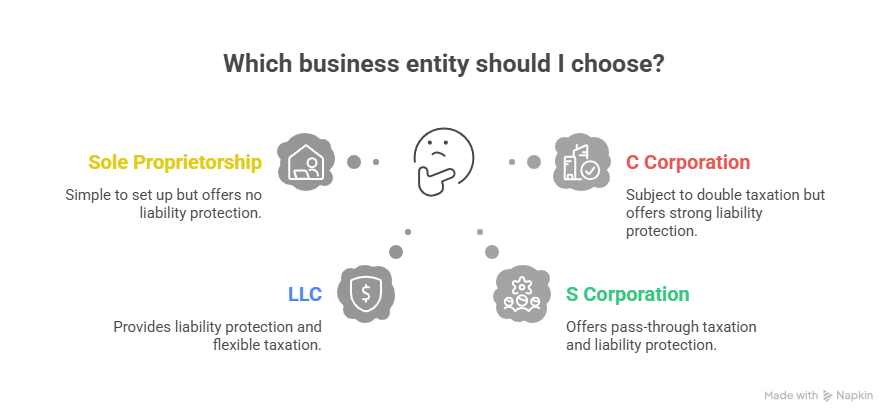

Entity Selection Influences Your Tax Exposure

Your entity choice affects how income flows to you and how taxes are assessed.

Common options include:

- Sole proprietorship.

- Limited Liability Company.

- S Corporation.

- C Corporation.

Each structure carries different implications for income tax, payroll tax, and state obligations. For example, S corporation elections may reduce self-employment tax exposure, while C corporations may benefit startups planning venture capital funding.

Choosing incorrectly can increase tax burden or complicate ownership transitions. Early consultation with a startup tax accountant ensures your structure aligns with projected revenue and growth goals.

Deducting Startup Costs Properly

Many founders do not realize that startup costs incurred before operations begin are treated differently from ordinary business expenses.

You may claim up to $5,000 in startup expenses in your first year, subject to limitations. Remaining costs are amortized over 15 years.

Eligible startup expenses may include:

- Market research.

- Legal formation fees.

- Pre-opening advertising.

- Professional consulting.

Proper categorization ensures compliance while maximizing allowable deductions.

Complying With State Tax and Reporting Obligations

Beyond federal taxes, startups must consider state-level requirements.

Some states impose minimum annual franchise taxes, even if your business generates little or no income. Overlooking these obligations can result in unexpected notices and penalties.

Strategic planning around franchise tax obligations ensures your startup remains in good standing.

State compliance includes annual reports, registered agent requirements, and minimum fee payments. These recurring obligations should be integrated into your financial planning from the start.

Estimated Taxes and Cash Flow Forecasting

Unlike W-2 employees, founders are typically responsible for making quarterly estimated tax payments.

Failing to pay sufficient estimates can result in underpayment penalties.

Startup tax services include:

- Calculating projected taxable income.

- Estimating federal and state tax liability.

- Aligning payment schedules with revenue patterns.

When estimates are calculated accurately, you avoid surprises and protect working capital.

Payroll Compliance and Early Hiring Decisions

Once you hire employees, payroll taxes become part of your compliance responsibilities.

This includes:

- Withholding federal and state income taxes.

- Paying employer payroll taxes.

- Filing quarterly returns.

- Issuing year-end forms.

Managing quarterly payroll filing properly reduces penalty risk and maintains regulatory compliance.

Additionally, worker classification between employees and independent contractors must be handled carefully. Misclassification can lead to back taxes and legal exposure.

Research and Development Credits for Eligible Startups

Many innovative startups qualify for Research and Development tax credits but fail to claim them.

Eligible activities may include:

- Developing proprietary software.

- Creating new manufacturing processes.

- Improving existing products.

The R&D credit can offset payroll taxes in certain cases, providing immediate financial benefit even before profitability.

An experienced startup tax provider can evaluate whether your business activities meet qualification criteria.

Equity Compensation and Tax Planning

If you issue stock options or equity incentives, tax treatment becomes more complex.

You must consider:

- Vesting schedules.

- Taxable events upon exercise.

- Alternative Minimum Tax implications.

- Reporting requirements.

Improper handling of equity compensation can create unexpected tax liabilities for both you and your employees.

Structured tax preparation for startups ensures equity decisions are aligned with the overall financial strategy.

How Can You Avoid Common Startup Tax Filing Mistakes

Startup tax filing involves multiple forms, including entity returns and personal returns for pass-through income.

Common mistakes include:

- Failing to file required state returns.

- Missing entity election deadlines.

- Misreporting owner distributions.

- Ignoring depreciation schedules.

Accurate filing protects your business from penalties and strengthens credibility with investors and lenders.

Comparing Reactive and Proactive Startup Tax Services

| Approach | Reactive Filing | Proactive Planning |

| Timing | Once per year | Year-round |

| Tax Strategy | Limited | Strategic |

| Cash Flow Planning | Minimal | Structured |

| Compliance Monitoring | Basic | Ongoing |

| Risk Management | Moderate | Strengthened |

When to Engage a Startup Tax Provider

Many founders wait until tax season to seek assistance. However, the most valuable tax decisions are made before year-end.

You should consider engaging professional support if:

- Your revenue is increasing rapidly.

- You are hiring employees.

- You are considering an entity election.

- You are seeking outside funding.

- You operate in multiple states.

Ongoing tax services for startups reduce uncertainty and improve long-term financial efficiency.

Wrap-Up

If you want to lower taxes early while protecting compliance, make your move now. Strategic startup tax services can help you build a strong financial foundation that supports growth instead of limiting it.

Arrange a one-on-one consultation with Houston CPA Zahra Samji today! She will thoroughly go through your entity structure, projected income, and payroll setup to create a proactive tax plan tailored to your startup.

Startup Tax Services FAQs

- When should I hire a startup tax accountant?

Ideally, before launching operations. Early planning ensures correct entity selection, deduction tracking, and compliance registration.

- Are tax services for startups different from regular business tax services?

Yes. Startups face quick expansion, funding preparation, R&D credits, and unique equity compensation considerations that require specialized planning.

- Can a startup tax provider help reduce payroll taxes?

Yes. Strategic entity elections, compensation planning, and available credits may reduce overall payroll tax exposure.

- What does tax preparation for startups include?

Tax preparation for startups includes filing federal and state returns, reviewing financial records for accuracy, ensuring proper deductions, and aligning reported income with accounting records.