Most small business owners think about taxes once a year. The ones who consistently keep more of their revenue think about them all year long.

Effective small business tax planning is not about finding loopholes, but it is about making well-timed decisions that reduce your liability within the full bounds of the tax code.

This blog covers the strategic angles that get overlooked most often, so your tax position works for your business instead of against it.

Why Your Entity Structure Is a Tax Planning Decision

The way your business is structured has a direct impact on how much self-employment tax you pay, how profits are distributed, and what deductions are available to you. Many small business owners choose their entity type at formation and never revisit it, even as their income grows significantly.

If you are operating as a sole proprietor or single-member LLC, all of your net profit is subject to self-employment tax at 15.3% on the first $182,700 in 2026.

Electing S Corporation status allows you to divide your income into a reasonable salary and a distribution. Only the salary portion is subject to payroll taxes, which means the distribution portion avoids that 15.3% hit entirely.

This is not a strategy that works for every income level. It makes the most financial sense when your net profit is high enough that the payroll tax savings outweigh the administrative costs of running an S Corp.

A licensed CPA, like Zahra Samji at Skyline Financial, can help you model the numbers before you make that election because once it is filed, it is difficult to reverse.

Timing Your Income and Expenses to Control Your Tax Bracket

One of the most underutilized tools in small business tax planning is the strategic timing of income recognition and expense deductions. You have more control over this than you think, particularly if your business operates on a cash basis.

Here is how timing decisions work in practice:

- If you expect a lower-income year ahead, deferring invoices to January shifts that income into the next tax year and keeps your current-year bracket lower.

- If you expect a higher income in the year ahead, accelerating deductible expenses into the current year reduces what you owe now.

- Large equipment purchases can be fully expensed in the year of purchase under Section 179 or bonus depreciation, rather than being depreciated over several years.

- Prepaying certain business expenses like insurance premiums, software subscriptions, or rent before year-end can pull those deductions into the current tax year.

The key is that these decisions need to happen before December 31st. Once the calendar year closes, your options narrow considerably.

Retirement Contributions as a High-Leverage Tax Reduction Strategy

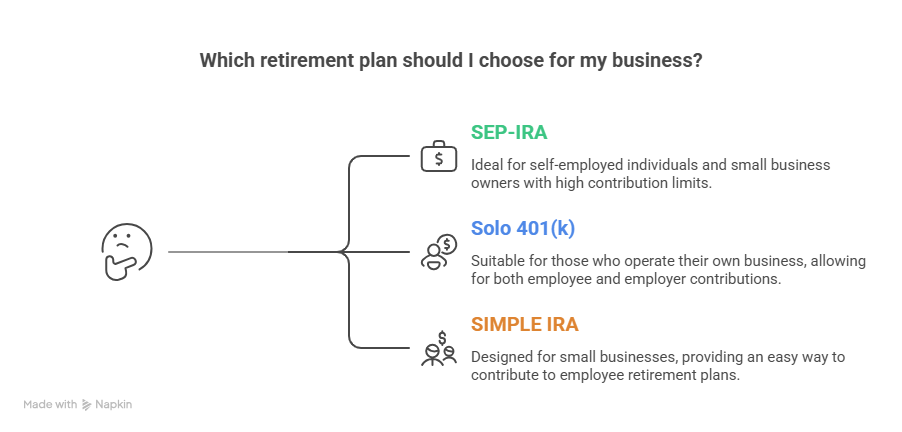

If you are not using a retirement plan to reduce your taxable income, you are leaving one of the most powerful tools in the tax code completely unused.

For self-employed individuals and small business owners, the options go far beyond a standard IRA:

- SEP-IRA: Allows contributions of up to 25% of net self-employment income, with a 2026 maximum of $72,000. Contributions are fully deductible.

- Solo 401(k): Available to owner-only businesses, allowing both employee and employer contributions for a combined maximum of $72,000 (or $79,500 if you are 50 or older).

- SIMPLE IRA: Designed for businesses with employees, with lower contribution limits but simpler administration.

Each of these plans plays a key role in small business tax planning Houston TX by reducing your taxable income per dollar. A SEP-IRA contribution of $20,000, for example, reduces your federal taxable income by $20,000 with the added benefit of building long-term wealth at the same time.

The Qualified Business Income Deduction and Who Actually Benefits From It

The Section 199A qualified business income (QBI) deduction allows approved pass-through business owners to deduct up to 20% of their qualified business income. It is one of the most significant deductions available to small businesses, yet many owners do not claim it or do not structure their businesses to maximize it.

Eligibility phases out for certain service businesses, including financial services, consulting, and law, once taxable income exceeds $203,000 for single filers and $406,000 for joint filers in 2026.

If your income is approaching those thresholds, proactive small business tax planning can bring your taxable income below the phase-out range and preserve the deduction.

| Strategy | Tax Impact |

| S Corp election | Reduces self-employment tax on distributions |

| Section 179 expensing | Accelerates equipment deductions to the current year |

| SEP-IRA or Solo 401(k) | Reduces taxable income dollar for dollar |

| QBI deduction optimization | Deducts up to 20% of qualified business income |

| Income and expense timing | Controls which tax year liability falls into |

Final Word

Effective small business tax planning is the difference between reacting to your tax bill and actively managing it. Each strategy covered in this blog represents a real opportunity to reduce what you owe and keep more of what you earn.

At Skyline Financial CPA in Houston, Zahra Samji works directly with Houston small business owners to build tax strategies that are specific to their income, entity type, and financial goals.

If you want clarity on where your biggest opportunities are, schedule a consultation with her now!

FAQs

When is the best time to start small business tax planning?

The best time is at the start of your fiscal year, with check-ins each quarter. Waiting until tax season limits your options significantly since most strategies require action before December 31st.

How do I know if an S Corp election makes sense for my business?

It typically makes sense when your net profit is high enough that the payroll tax savings on distributions exceed the administrative costs of running the S Corp. A CPA can model the break-even point for your specific income level.

Can I still make retirement contributions after December 31st?

SEP-IRA contributions can be made up to your tax filing deadline, including extensions. Solo 401(k) contributions generally require the plan to be established before December 31st of the tax year.

What is the Texas franchise tax No Tax Due threshold?

For the 2026 report year, most entities with annualized total revenue below $2.65 million qualify for the No Tax Due threshold. A report still needs to be filed even when no tax is owed.

Does the QBI deduction apply to all small businesses?

It applies to most pass-through businesses, but service-based businesses face income phase-outs. Proactive planning around those thresholds can help preserve the deduction even as income grows.