Filing the S Corp election form can be one of the most strategic tax decisions you make for your business. When completed correctly, IRS Form 2553 allows your company or LLC to be taxed as an S Corporation, potentially reducing self-employment taxes and improving overall tax efficiency. However, mistakes, missed deadlines, or incomplete information can delay approval or create compliance issues.

If you are considering this election, you need more than basic instructions. You need clarity on eligibility, timing, compensation rules, and long-term tax impact.

Let’s walk through how you can file correctly and avoid common pitfalls.

What Does the S Corp Election Really Change?

Electing S Corporation status does not change your legal entity. It changes how your business is taxed.

Without the election, a single-member LLC is taxed as a sole proprietorship by default. A multi-member LLC is subject to tax as a partnership. Once you file Form 2553 and receive approval, your entity becomes a pass-through entity taxed under Subchapter S of the Internal Revenue Code.

This impacts:

- How profits are reported.

- How owner compensation is treated.

- How payroll must be structured.

- How distributions are taxed.

The S Corporation election form is not just paperwork. It triggers ongoing compliance responsibilities that must be handled correctly.

Deciding If You Qualify Before Filing

Not every business meets the requirements for S Corporation status. Before filing, you must confirm that your entity meets IRS requirements, including:

- Domestic corporation or eligible LLC.

- No more than 100 shareholders.

- Shareholders need to be U.S. citizens or residents.

- Only one class of stock.

If your ownership structure is complex or you anticipate bringing in investors, eligibility should be evaluated carefully before submission.

Key Deadlines You Cannot Afford to Miss

One of the most common errors with the S Corp election form is missing the filing deadline.

To be effective for the current tax year, Form 2553 must generally be filed:

- Within two months and 15 days after the beginning of the tax year.

- Or at any time during the preceding tax year.

If your business operates on a calendar year, that typically means filing by March 15.

Late elections are sometimes accepted, but relief is not automatic. You must provide reasonable cause for the delay and meet specific IRS criteria.

Missing the deadline may postpone tax benefits for an entire year.

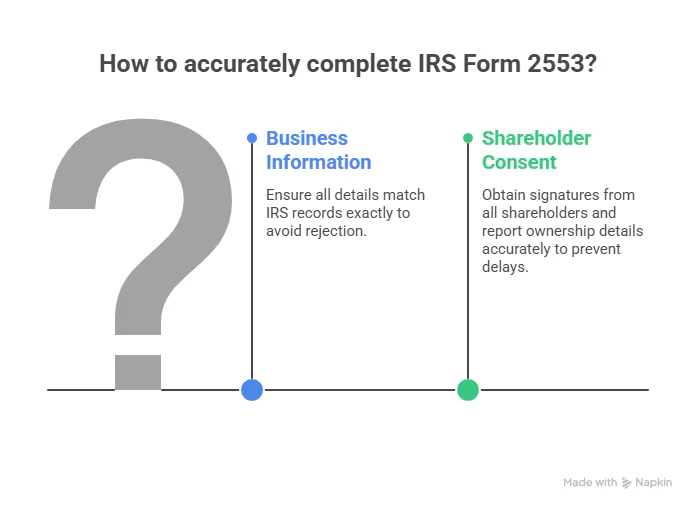

Important Steps to Complete Form 2553 Accurately

IRS Form 2553 requires detailed information. While it appears straightforward, small mistakes can lead to rejection or delays.

Business Information Section

You must include:

- Legal entity name.

- EIN

- Business address.

- Date of incorporation or formation.

- State of formation.

Make sure that the information matches IRS records exactly.

Shareholder Consent Section

All shareholders must sign the form. Missing signatures are a common reason for rejection.

You must also report:

- Ownership percentage.

- Number of shares.

- Date shares were acquired.

Any discrepancy in ownership records can trigger IRS questions.

Reviewing The Tax Year Selection Carefully

Most businesses use a calendar year. However, fiscal year elections require additional justification and may require IRS approval.

If your selected tax year does not align with your operational reality, it can create complications in financial reporting and compliance.

This is an area where professional oversight becomes particularly valuable.

Compensation Rules After Approval

Filing the S Corp election form is only the beginning. Once approved, you must comply with reasonable compensation requirements.

As an owner actively working in the business, you are required to:

- Pay yourself a reasonable salary.

- Withhold payroll taxes.

- File payroll tax returns.

- Issue a W-2.

Failure to pay reasonable compensation is one of the most frequently occurring audit triggers for S Corporations.

Distributions taken in excess of salary may be reclassified by the IRS, resulting in penalties and back payroll taxes.

Payroll Setup And Compliance Planning

Many guides stop at filing Form 2553. However, operational adjustments are equally important.

After approval, you must:

- Register for state payroll accounts.

- Set up payroll processing.

- Track salary versus distributions.

- File quarterly payroll tax returns.

If you transition mid-year, additional coordination is required to ensure payroll is handled correctly from the effective date forward.

For more guidance, reach out to our Houston CPA, Zahra Samji, who can help you with the S Corporation election and clarify post-approval obligations.

Comparing Tax Impact Before Filing

Before submitting the S Corp election form, you should analyze projected tax savings.

Key considerations include:

- Net business income.

- Current self-employment tax liability.

- Reasonable salary expectations.

- Administrative payroll costs.

Below is a simplified comparison:

| Tax Factor | Default LLC Taxation | S Corporation Taxation |

| Self-employment tax | Applied to all net profit | Applied only to salary |

| Payroll requirement | Not required | Required |

| Administrative complexity | Lower | Higher |

| Potential tax savings | Limited | Possible with proper structure |

Avoiding Common Filing Mistakes

The most frequent errors include:

- Missing shareholder signatures.

- Incorrect EIN or entity name.

- Filing after the deadline without explanation.

- Failing to set up payroll after approval.

- Misunderstanding the effective date.

You should also retain confirmation from the IRS. If you do not receive written approval, follow up immediately.

Proper documentation protects you in case of future compliance questions.

Final Thoughts

Filing the S Corp election form is a strategic decision that affects your taxes, payroll structure, and long-term compliance obligations. When handled correctly, it can reduce self-employment taxes and improve financial efficiency. When handled incorrectly, it can create costly complications.

If you are considering S Corporation status or are unsure whether your Form 2553 was completed properly, Skyline Financial CPA Houston can review your eligibility, analyze projected savings, and ensure your filing meets IRS requirements. Call today to schedule a consultation!

S Corp Election Form FAQs

- What happens if I miss the Form 2553 deadline?

You may qualify for late election relief, but you must demonstrate reasonable cause and meet IRS criteria.

- Do I need to change my LLC to a corporation before filing?

No. An LLC can elect S Corporation tax status without changing its legal structure.

- How long does IRS approval take?

Approval typically takes several weeks. You should receive written confirmation from the IRS.

- Can I revoke S Corporation status later?

Yes. However, revocation has tax consequences and may limit future elections.

- Is S Corporation status always beneficial?

Not necessarily. Tax savings depend on profit level, salary structure, and administrative costs.