How long should you keep tax returns and all your supporting documents? The answer is different for everyone. The IRS may want you to keep some tax records for a few years or even forever. This depends on your situation.

At Skyline Financial Houston CPA, we know that keeping things organized saves you a lot of stress. It helps if you face audits, need to file an amended return, or apply for a loan.

In this guide, we will show you how long to keep your tax documents. We will also explain which ones you should save. Plus, we will tell you when it’s safe to let go of old files.

Why You Should Keep Your Tax Returns

Keeping your income tax returns and supporting documentation is more than just following the rules. It’s your financial safety net. Your tax return records show what you filed, what you earned, and the credits or deductions you claimed.

These documents are very important if you ever need to file an amended return. They are also helpful if you want to apply for a tax credit. Plus, you will need them to prove your income for a mortgage or a business loan.

The IRS has specific rules for how long you should keep different records. Let’s go through them so you can stay confident and compliant.

The General Rule For How Long Should You Keep Tax Returns

In general, the IRS tells you to keep your tax returns and records for at least three years from the day you filed your return. Or, keep them for two years from the day you paid the tax, whichever is later.

But it can get a bit confusing. You might need to keep some records longer depending on your tax situation. Let’s look at the exceptions so you know exactly what to do.

1. When to Keep Tax Returns for 3 YearS

Most taxpayers fall into this group. You should keep your income and expense records, W-2s, 1099s, receipts, and cancelled checks for three years.

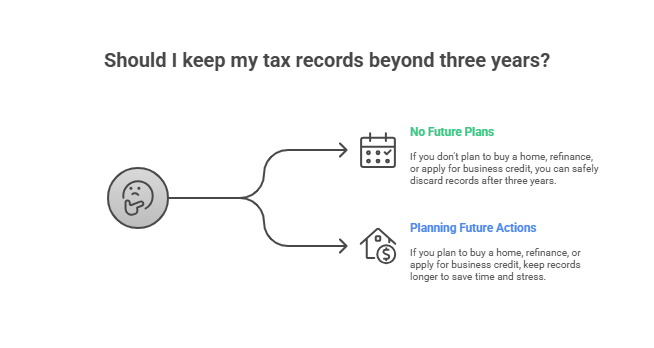

Why three years? That’s how long the IRS usually has to audit your tax year or question your gross income. If you reported everything correctly and don’t plan to file an amended return, you can safely toss your records after that.

But before you shred anything, ask yourself this:

● Are you planning to buy a home soon?

● Do you want to refinance?

● Or are you thinking about applying for business credit?

If yes, keeping your records a little longer can save you time and stress.

2. When to Keep Tax Returns for 6 Years

The IRS can audit you for up to six years if your reported gross income is more than 25% too low. In that case, keep your tax documents and supporting documentation for at least that long.

The same goes if you earn money from self-employment and have multiple income sources. Keeping complete records of employment tax records, business expenses, and receipts helps you prove every claim if needed.

Skyline Financial Management can help if you are not sure how to handle your self-employment records. We are here to offer self-employment tax services to help you file correctly.

3. When to Keep Tax Returns for 7 Years

Did you claim a bad debt deduction or report a loss from worthless securities? If so, you might be wondering, How long should you keep tax returns. The IRS says you should keep these records for seven years.

Keeping them longer gives you proof if the IRS reviews your tax year in the future. It also helps if you need to show your financial history for business deals or investments. Having these tax documents ready makes things much easier when you need them.

4. When You Should Keep Tax Returns Indefinitely

Some records are worth keeping forever. You should hold onto your tax returns indefinitely if:

● You didn’t file a return at all.

● You filed a fraudulent return.

● You have ongoing gain or loss tracking, like property or investments.

For example, if you own real estate or stocks, keep all purchase and sale documents until you sell the asset. After that, keep the related tax return for several more years. This way, you always have the proof you might need.

5. Employment Tax Records for Businesses

You need to keep employment tax records if you own a business or have employees. Hold onto them for at least four years after the tax is due or paid.

These records include employee earnings, W-4 forms, payroll reports, and tax deposits. Many businesses make the mistake of throwing them away too soon. This can cause problems during an audit or when you need to verify benefits.

At Skyline Financial Management, we help small business owners and franchise operators keep their records organized. Our franchise tax services make sure you stay IRS-compliant and avoid unnecessary stress.

How Long to Keep Other Financial Documents

You might be thinking about other documents beyond your tax returns. Let’s take a look at some common tax documents and other records and see how long you should hold onto each. This way, you stay organized and ready if you ever need them.

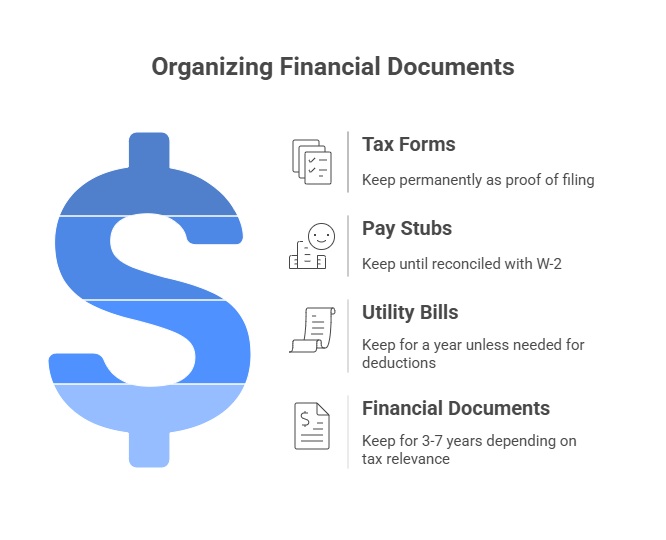

● How long to keep tax forms:

You should keep copies of your actual filed forms, like 1040s, W-2s, and 1099s, permanently. These tax documents act as proof that you filed your taxes. You never know when you might need them for audits, loans, or other financial matters. Keeping them makes your life easier.

● How long should you keep pay stubs:

Keep your pay stubs until you make sure they match your year-end W-2. Once you have checked and everything lines up, you can safely throw them away. This helps you stay organized without holding onto unnecessary tax documents.

● How long to keep utility bills:

You can throw them away after a year unless you need them to prove deductions for a home office or rental property. Keeping them longer isn’t usually necessary. Only hold onto them until the IRS can no longer question that year’s return.

● How long to keep financial documents:

You should keep bank statements, investment records, and loan documents for at least three to seven years. How long depends on how they relate to your taxes. Keeping these tax documents helps you prove income, expenses, or deductions if the IRS ever has questions. It also makes it easier to track your financial history.

Remember, the answer to how long should you keep tax returns can change depending on your case. It’s safer to keep your tax documents a little longer if you are not sure. This way, you won’t have to worry if the IRS asks for them later.

What’s Best for Record-Keeping?

You don’t have to keep piles of paper. The IRS lets you use electronic copies of your tax records as long as they are clear and easy to access.

You can scan receipts, bank statements, and supporting documentation. Store them neatly in folders on your computer or in the cloud. Make sure your backups are safe and easy to get to in case of an IRS audit.

At Skyline Financial Management, we suggest creating a simple system. Name files by tax year and use folders for categories like income, deductions, and tax credit claims. This makes it easy for you to find what you need, when you need it.

When to Discard Old Tax Records Safely

It’s safe to shred old paper files once you have kept your tax documents for the required time. You can also delete digital copies securely.

Identity theft is real, so don’t let sensitive information like your Social Security number or account details fall into the wrong hands.

Before you throw anything away, double-check that you:

● Don’t need the records for ongoing gain or loss tracking.

● Aren’t waiting on a file, an amended return, or an IRS response.

● Don’t need them for loans, mortgages, or insurance purposes.

We can review your records for you if you are unsure. We will help you build a safe, organized plan for keeping your tax documents through our individual tax services.

Practical Tips for Smart Tax Record Organization

Here are some tips to keep your tax documents organized:

1. Make annual folders for each tax year, both on your computer and in paper files.

2. Keep personal and business expenses separate. This avoids confusion later.

3. Store important records off-site or in the cloud for backup.

4. Label your files clearly. Use keywords like “2025 Income Statements” or “2025 Deductions.”

5. Check your records every year and decide what to keep or throw away.

Being organized doesn’t just save you time. It also protects you if the IRS ever audits your tax documents or you need proof for a financial review.

Why Working With Skyline Financial Management Helps

At Skyline Financial Management, we know that keeping good records is key to healthy finances. We help you stay organized, follow the rules, and be ready in case of an audit.

We can guide you if you need help understanding how long should you keep tax returns. We can also help you manage your digital files. And we will make sure your tax documents match IRS standards. We’re here to walk you through everything.

We handle it all. This includes individual tax services, S-corp, self-employment, and franchise tax support. We also offer other solutions that are all made to match your needs.

Need help getting your tax records in order or tax preparation Houston TX for the next tax season? Contact Skyline Financial CPA Houston today and let us guide you from beginning to end!

FAQs

1. How long should you keep tax returns if you have investments or property?

You should keep your records until you sell the asset, and then keep them for at least three more years. This way, you can figure out the gain or loss correctly and have proof if the IRS checks your case.

2. Can I store tax returns digitally instead of keeping paper copies?

Yes, you can store your tax documents electronically. They just need to be accurate, easy to read, and easy to access when you need them. Using secure cloud storage is a smart option.

3. Do I need to keep old utility bills or pay stubs?

You can throw away utility bills after a year unless you need them for deductions. Pay stubs can be discarded once you make sure they match your W-2 for that tax year.

4. How long to keep records if I need to file an amended return?

You should keep your records for at least three years after you file it if you file an amended return. Or keep them for two years after you pay the tax.

5. What happens if I discard my tax returns too early?

You can run into problems if the IRS audits you and you’ve thrown away your income tax returns or supporting documentation. You might have trouble proving your deductions or your income.

Final Thoughts

Understanding how long should you keep tax returns isn’t just about following the rules. It’s about protecting your financial future.

You can keep your tax documents, receipts, and records organized to make audits easier. It also speeds up loan approvals. Plus, it gives you complete calm and reassurance.

At Skyline Financial Management, we support individuals and businesses with reliable payroll services Houston TX, accurate Houston bookkeeping services, and comprehensive accounting services Houston. Our proactive tax planning Houston TX strategies also help you stay compliant while minimizing liabilities and preparing for long-term growth.

Are you ready to make record-keeping easy and stress-free? Contact Skyline Financial Management today for expert tax guidance and professional financial management.