Running payroll looks simple from the outside. Employees work, and you pay them.

But the compliance obligations layered underneath every paycheck make payroll one of the most penalty-sensitive functions in your entire business operation.

If you have been asking how do payroll services work and whether they are worth the investment, the answer starts with understanding what actually happens between collecting time data and issuing a direct deposit.

This blog walks you through the full payroll workflow, the compliance checkpoints, and the specific areas where errors create the most financial exposure for small business owners.

The Data Collection Stage That Determines Everything Downstream

Every payroll run starts with data, and the accuracy of everything that follows depends entirely on what goes in at this stage. Before a single calculation is made, a payroll system needs to know who worked, for how long, at what rate, and under what classification.

For hourly employees, that means time and attendance records that are complete, approved, and reconciled against scheduled hours. For salaried employees, the focus shifts to verifying that any mid-period changes to compensation, benefits elections, or deductions are captured before the run begins.

The data inputs that feed every payroll calculation include:

- Employee classification as hourly, salaried, or exempt versus non-exempt under the Fair Labor Standards Act.

- Current pay rates, including any mid-period adjustments, bonuses, or commission payments.

- Hours worked, including regular time, overtime at the applicable multiplier, and any paid time off used.

- Benefit deductions for health insurance, retirement contributions, and flexible spending accounts.

- Garnishment orders for child support, tax levies, or creditor judgments must be processed before net pay is issued.

- Form W-4 withholding elections for each employee, which determine federal income tax withholding amounts.

How Do Payroll Services Work Through the Gross-to-Net Calculation

Once data is confirmed, the payroll system performs the gross-to-net calculation that produces each employee’s actual take-home pay.

Here is what the calculation sequence looks like:

| Step | What Is Being Calculated |

| Gross pay | Total earnings before any deductions |

| Pre-tax deductions | 401(k) contributions, HSA, FSA, and employer health premiums |

| Federal income tax withholding | Calculated from W-4 elections and IRS withholding tables |

| Social Security withholding | 6.2% of gross pay up to the annual wage base |

| Medicare withholding | 1.45% of gross pay, plus 0.9% for earnings over $200,000 |

| State income tax withholding | Applicable in states with income tax (not applicable in Texas) |

| Post-tax deductions | Roth 401(k) contributions, garnishments, and voluntary deductions |

| Net pay | Amount deposited or paid to the employee |

The Tax Deposit and Filing Obligations That Run Parallel to Every Payroll Run

Understanding how do payroll services work from a compliance perspective means looking beyond employee pay and focusing on obligations to the IRS after each run.

Every payroll creates tax deposit obligations, including withheld federal income tax and both shares of Social Security and Medicare. New employers typically start with monthly deposits due by the 15th, moving to semi-weekly as liability exceeds $50,000.

Quarterly payroll filings add another layer. Form 941 reports wages, taxes, and deposits, and staying current ensures your filings match your payments, which is one of the first things the IRS reviews.

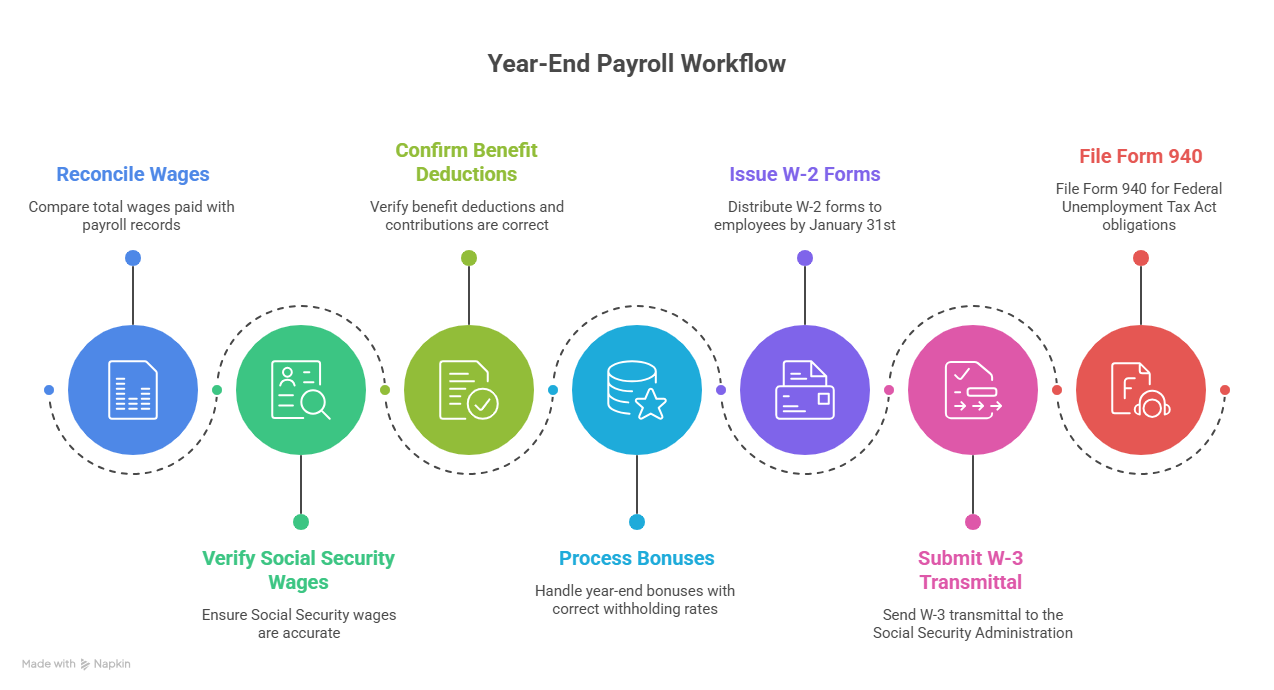

The Year-End Payroll Workflow That Most Business Owners Underestimate

The end of the calendar year triggers a separate layer of payroll obligations that extends well beyond the final payroll run of December. This stage is where accumulated errors in employee data, withholding calculations, and benefit deductions become visible and where corrections need to happen before forms are issued.

The year-end payroll workflow includes:

- Reconciling total wages paid against cumulative payroll records to confirm accuracy across all pay periods.

- Verifying that Social Security wages are correct and that the wage base cap was applied properly for high earners.

- Confirming that all benefit deductions and employer contributions are accurately reflected across the year.

- Processing any year-end bonuses with the correct supplemental withholding rates applied.

- Issuing W-2 forms to all employees by January 31st with accurate figures for wages, withheld taxes, and benefit contributions.

- Submitting the W-3 transmittal to the Social Security Administration along with copies of all W-2s.

- Filing Form 940 for Federal Unemployment Tax Act obligations based on wages paid during the year.

A single error in this sequence produces incorrect W-2s that require corrections, which triggers amended returns for affected employees and additional IRS correspondence for your business.

Last Thoughts

Being familiar with how do payroll services work gives you the foundation to manage this function with confidence rather than anxiety.

From data collection and gross-to-net calculations to tax deposits, quarterly filings, and year-end reporting, every stage of the payroll workflow carries compliance weight that accumulates into your overall tax position.

Working with Zahra Samji at Skyline Financial CPA Houston TX means bringing clarity to payroll obligations, filing requirements, and the tax implications that connect payroll decisions to your broader financial strategy.

If you want to make sure your payroll process is accurate, compliant, and aligned with your tax position, schedule a consultation today and connect with her for your payroll services Houston TX.

Your employees and your compliance record both deserve that standard of care!

How Do Payroll Services Work FAQs

How do payroll services work for businesses with both salaried and hourly employees?

The system handles both classifications simultaneously, applying hourly rate calculations and overtime rules for hourly staff while processing fixed compensation for salaried employees, all within the same payroll run.

How often should payroll be run for a small business?

Most small businesses run payroll biweekly or semi-monthly. The frequency affects your cash flow planning and deposit schedule, so consistency matters as much as the interval you choose.

What is the difference between Form 941 and Form 940?

Form 941 is filed quarterly and reports federal income tax withheld plus Social Security and Medicare taxes. Form 940 is filed annually and covers Federal Unemployment Tax Act liability based on total wages paid during the year.

Can payroll services handle tip reporting for restaurant or hospitality businesses?

Yes. Tips are subject to the same withholding and reporting requirements as regular wages. Payroll systems built for service industries can incorporate reported tip amounts into the gross-to-net calculation and Form 8027 annual tip reporting.

What records should I keep after each payroll run?

Retain payroll registers, tax deposit confirmations, Form 941 copies, and employee time records for at least four years. The IRS can assess payroll tax liability within that window, so complete documentation is your primary defense.