If you opened your tax return expecting a refund but instead found a balance due, your first reaction was likely frustration. You may be asking yourself, why do I owe state taxes? The answer is rarely simple. State tax balances usually result from withholding miscalculations, income changes, residency issues, or ignored reporting requirements.

Unlike federal returns, state tax systems vary widely. Each state has its own rules regarding income thresholds, deductions, credits, and withholding formulas. Understanding why you owe is the first step toward preventing the same issue next year.

Let’s walk through the most common causes and how you can correct them.

Why Do You Owe State Taxes When You Received a Federal Refund?

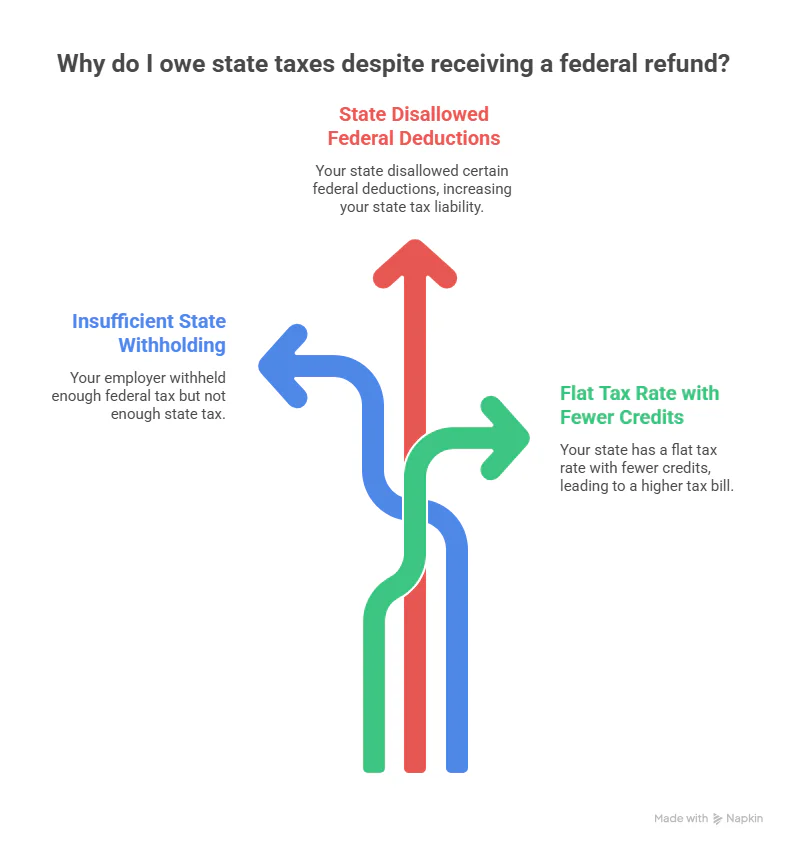

It is possible to receive a federal refund while still owing your state. This happens because federal and state tax systems operate independently.

Your federal withholding does not guarantee sufficient state withholding. In some cases:

- Your employer withheld enough federal tax but not enough state tax.

- Your state disallowed certain federal deductions.

- Your state has a flat tax rate with fewer credits.

The mismatch between federal and state withholding often surprises taxpayers who assume both systems align perfectly.

Insufficient State Withholding From Your Paycheck

One of the most common answers to the question “Why do I owe state taxes?” is simple underwithholding.

State withholding depends on:

- Your state W-4 equivalent form.

- Filing status.

- Claimed allowances.

- Additional income.

If you changed jobs, received a raise, or adjusted allowances without updating state withholding forms, your payroll deductions may not reflect your actual tax liability.

Reviewing your pay stub can help you determine whether enough state tax is being withheld each pay period.

Multiple Jobs or Household Income Coordination Issues

If you or your spouse holds multiple jobs, withholding may be calculated independently at each employer without accounting for combined income.

This can result in:

- Lower withholding at each job.

- Underestimated total taxable income.

- Higher effective state tax liability.

Many payroll systems assume a single income source. Without adjustments, combined earnings may push you into a higher bracket than anticipated.

You may need to request additional withholding to offset this gap.

Self-Employment and Estimated Payment Gaps

If you earn freelance or business income, no taxes are automatically withheld unless you make estimated payments.

Common mistakes include:

- Underestimating quarterly state tax payments.

- Forgetting to file state estimated payments altogether.

- Assuming federal estimated payments cover state obligations.

State estimated taxes are separate from federal payments. If you are self-employed and not calculating state liability accurately, you may face both taxes due and penalties.

Residency Changes and Part-Year Filing Complications

Moving between states during the year often triggers unexpected balances.

If you relocated, you may need to:

- File part-year resident returns in both states.

- Allocate income properly between jurisdictions.

- Adjust withholding for the new state.

Improper allocation of income can result in double taxation or underpayment.

If you lived in one state and worked in another, reciprocal agreements may apply. However, not all states participate in these agreements.

Residency issues are frequently overlooked and can significantly affect your final balance.

Investment Income and Capital Gains Surprises

Investment income is another forgotten factor.

If you had:

- Capital gains from stock sales.

- Cryptocurrency transactions.

- Rental property income.

- Dividend income.

Your state tax liability may have increased, especially if no withholding applied to those gains.

Many taxpayers ask, “Why do I owe state taxes?” after selling assets without considering state-level capital gains taxation.

States often tax investment income differently from federal rates, and withholding rarely occurs automatically.

Credits and Deductions Not Available At The State Level

Federal and state deduction rules do not always match.

For example:

- Certain itemized deductions may be limited or disallowed.

- Federal credits may not apply at the state level.

- State standard deduction amounts may differ significantly.

If your state disallows deductions you claimed federally, your taxable income may be higher than expected.

Below is a simplified comparison:

| Factor | Federal Return | State Return |

| Standard deduction amount | Varies by filing status | Usually lower |

| Capital gains treatment | Preferential rates | May be taxed as ordinary income |

| Certain credits | Widely available | Limited or unavailable |

Why Do I Owe State Taxes After Moving or Working Remotely

Remote work has introduced new complexity.

If you worked remotely in a different state from your employer’s location, you may have:

- The withholding applied to the wrong state.

- Income sourced incorrectly.

- Missed required nonresident filings.

Remote arrangements sometimes create multi-state tax obligations that are not immediately obvious.

Proper sourcing rules establish which state has the right to tax your income.

How To Prevent Owing State Taxes Next Year

If you do not want to face the same issue next year, consider taking proactive steps:

- Review and adjust state withholding forms.

- Make quarterly estimated payments if self-employed.

- Track investment gains throughout the year.

- Consult before major financial transactions.

- Confirm residency classification after relocation.

Small adjustments now can prevent large balances later.

When Penalties and Interest Become A Concern

If you owe a significant amount, penalties may apply.

Common penalties include:

- Underpayment penalties.

- Late payment penalties.

- Interest accrual on unpaid balances.

Ignoring the issue can compound costs. If you already have an outstanding balance and need structured guidance, you can contact us to discuss next steps before penalties increase further.

Final Words

Why do I owe state taxes? The answer typically lies in withholding gaps, income changes, residency issues, or missed reporting requirements. State tax systems operate independently from federal rules, which means assumptions can lead to unexpected balances.

The key is proactive planning. Our professional Houston CPA, Zahra Samji, can help you gain clarity on your state tax liability and build a strategy to avoid future balances due. Book an appointment now!

FAQs

- Why do I owe state taxes but not federal?

State withholding may have been insufficient, or your state disallowed certain federal deductions.

- Can I set up a payment plan for state taxes?

Yes. Most states offer installment agreements, but interest may still apply.

- How do I adjust my state withholding?

You can submit an updated state withholding form through your employer’s payroll department.

- Do remote workers owe taxes in two states?

Possibly. It depends on residency status and state reciprocity agreements.

- Will owing state taxes affect my credit?

Generally, tax balances do not appear on credit reports immediately, but unpaid liabilities can escalate to collection actions if ignored.