If you invest in rental property, you’ve probably heard that a real estate professional status can give you major tax benefits. But qualifying is more detailed.

The IRS applies strict hour tests, documentation standards, and activity grouping rules that can affect your eligibility. When structured correctly, this designation can allow you to deduct rental losses from your ordinary income, potentially reducing your overall tax burden significantly.

At Skyline Financial CPA Houston, we guide property owners through these rules with clarity so you understand not just what qualifies but also how it applies to your specific situation.

Why Rental Losses Are Usually Limited

Rental activities are generally classified as passive under IRS rules. Passive losses typically can’t offset your W-2 wages, business income, or portfolio income. Instead, they’re carried forward to future years.

This is where qualifying changes everything.

If you meet the IRS criteria for real estate professional status, your rental activities are no longer automatically treated as passive. That shift allows eligible losses to offset other income sources, subject to additional material participation requirements.

But qualifying requires more than simply being “active” in your properties.

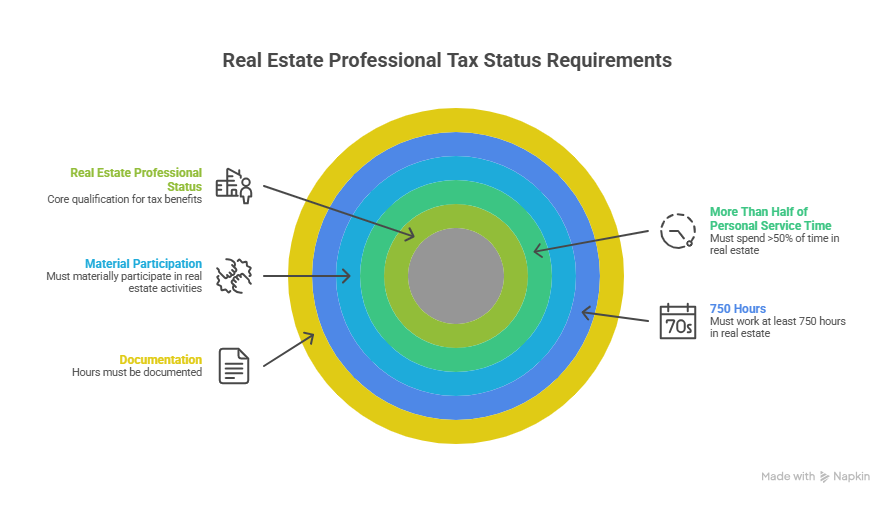

Real Estate Professional Tax Status Requirements You Must Meet

To qualify, you must pass two core IRS tests each year:

More Than Half of Your Personal Service Time Must Be in Real Property Trades

You must spend more than 50% of your total working hours in real property trades or businesses in which you materially participate.

This means:

- If you work a full-time W-2 job unrelated to real estate, qualifying becomes difficult.

- If real estate is your primary profession, your path is more straightforward.

Qualifying real property trades include:

- Development.

- Construction.

- Acquisition.

- Rental operations.

- Property management.

- Brokerage.

You Must Work at Least 750 Hours in Real Estate Activities

You must essentially participate in real estate activities for at least 750 hours during the tax year.

An important nuance is that these hours must be documented. Courts consistently rule against taxpayers who rely on estimates or reconstructed logs.

The Often-Overlooked Material Participation Standard

Meeting the hour thresholds alone is not enough. You must also prove material participation in each rental activity unless you elect to group them.

Material participation generally means:

- You are involved on a daily, continuous, and substantial basis.

- You make management decisions.

- You oversee operations, approve expenses, and coordinate contractors.

Many investors miss this detail. Without material participation, the IRS may still treat your rentals as passive even if you qualify under the main hour tests.

We often review time logs and operational involvement as part of our approach to handling complex real estate accounting Houston matters to ensure compliance is defensible.

Grouping Election Can Make or Break Your Eligibility

One advanced strategy is the grouping election under IRC Section 469.

Without grouping:

- Each rental property is viewed as a separate activity.

- You must materially participate in each one.

With grouping:

- All rental properties are treated as a single activity.

- Your total participation hours apply collectively.

This election must be formally made and properly disclosed. Failing to document it correctly can create audit exposure later.

If you own multiple properties, this decision alone can determine whether you benefit from real estate professional status or not.

Strategic Real Estate Professional Tax Benefits You Can Receive

When structured correctly, the tax advantages can be substantial.

Deduct Rental Losses Against Active Income

Instead of carrying losses forward, you may offset:

- W-2 wages.

- Self-employment income.

- Business profits.

For high-income taxpayers, this can create meaningful cash flow savings.

Accelerated Depreciation Benefits

When combined with cost segregation studies, you may:

- Front-load depreciation deductions.

- Offset substantial income in early ownership years.

The combination of depreciation acceleration and qualifying status can significantly lower taxable income.

Avoiding the Net Investment Income Tax Impact

Passive rental income may be subject to the 3.8% Net Investment Income Tax. Recharacterizing rental activities through qualification can change how this applies depending on your situation.

Because these strategies interact with broader tax planning, Skyline Financial CPA integrates them carefully within your full tax profile when addressing real estate tax planning and compliance.

A Clear Comparison of Passive vs Qualified Treatment

| Feature | Passive Rental Activity | Qualified Real Estate Professional |

| Losses Offset W-2 Income | No | Yes, if materially participating |

| 750 Hour Requirement | Not applicable | Required |

| More Than 50% Test | Not applicable | Required |

| Material Participation | Not required for passive classification | Required |

| Audit Scrutiny Level | Moderate | High if poorly documented |

Spousal Participation Rules Can Help You Qualify

If you file jointly, only one spouse must meet the hour tests. However, material participation can include combined spousal hours.

This means:

- One spouse may qualify under the 750-hour and 50% tests.

- Both spouses’ participation may count toward material participation for rentals.

This provision creates planning opportunities for married couples where one spouse transitions into real estate more actively.

Proper Documentation Protects Your Position

In tax court cases, inadequate documentation is the most common reason taxpayers lose qualification.

Best practices include:

- Contemporaneous time logs.

- Calendar entries.

- Emails and contractor communications.

- Property management records.

- Mileage tracking.

Spreadsheets created after an audit notice are rarely persuasive.

If you intend to claim real estate professional status, documentation is not optional. It is your foundation.

Concluding Insights

Qualifying for real estate professional status can transform how your rental losses are treated and how much tax you ultimately pay. But it requires careful analysis, documentation, and strategic planning.

If you want clarity on whether you qualify and how to structure your rentals properly, our licensed Houston CPA, Zahra Samji, is here to help. Schedule a consultation with her today so she can review your hours, income profile, and property structure.

Real Estate Professional Status FAQs

- How strict is the 750-hour requirement?

It is strictly enforced. The IRS requires credible documentation, and courts often disallow estimated time records.

- Can I qualify for real estate professional tax status if I have a full-time W-2 job?

It is difficult because you must prove your real estate hours exceed 50% of your total working time. In most full-time employment situations, this threshold is challenging to meet.

- Do I need to qualify every year?

Yes. The tests apply annually. You must meet both hour requirements each tax year you claim the designation.

- Does property management count toward my hours?

Yes, if you are materially participating and actively involved in management decisions rather than being purely passive.

- Is this status automatically granted if I am a licensed real estate agent?

No. A license alone does not qualify you. You must still meet both the 750-hour and more-than-half-of-working-time tests.