If you’re preparing to sell property, one of your first questions is likely how to avoid capital gains tax on real estate without triggering IRS issues.

The good news is that the tax code provides several legitimate strategies if you plan correctly and apply them properly. The key is understanding which rules apply to your specific property type, holding period, and long-term investment goals.

Zahra Samji, our professional Houston CPA, helps you evaluate your sale before it happens, not after closing, because timing and structure determine how much you keep.

Primary Residence Exclusion Can Eliminate Gains Entirely

If you’re selling your primary residence, Section 121 of the Internal Revenue Code may let you exclude:

- Up to $250,000 of gain if single.

- Up to $500,000 if married filing jointly.

To qualify, you must:

- Have owned the home for at least two years.

- Have lived in the home for at least two of the last five years.

- Not have claimed the exclusion within the past two years.

This strategy is commonly misunderstood. Partial exclusions may apply if you sell due to job relocation, medical conditions, or unforeseen circumstances.

However, depreciation claimed after May 6, 1997, on a converted rental portion is not excludable. That portion may still be taxed.

Understanding this nuance is critical when exploring how to avoid capital gains tax on real estate in hybrid-use properties.

Can You Defer Capital Gains Tax Through a 1031 Exchange

If your property is held for investment or business purposes, a 1031 exchange is one of the most powerful real estate tax deferral tools available.

Under Section 1031, you may defer capital gains tax by reinvesting proceeds into like-kind property. This is not forgiveness. It’s a deferral, but it can compound wealth over time.

Strict requirements apply:

- Identify replacement property within 45 days.

- Close within 180 days.

- Use a qualified intermediary.

- Avoid taking constructive receipt of funds.

A common mistake is assuming you can close first and structure the exchange later. That is not allowed.

When properly executed, a 1031 exchange can significantly delay tax liability, especially for investors building long-term portfolios.

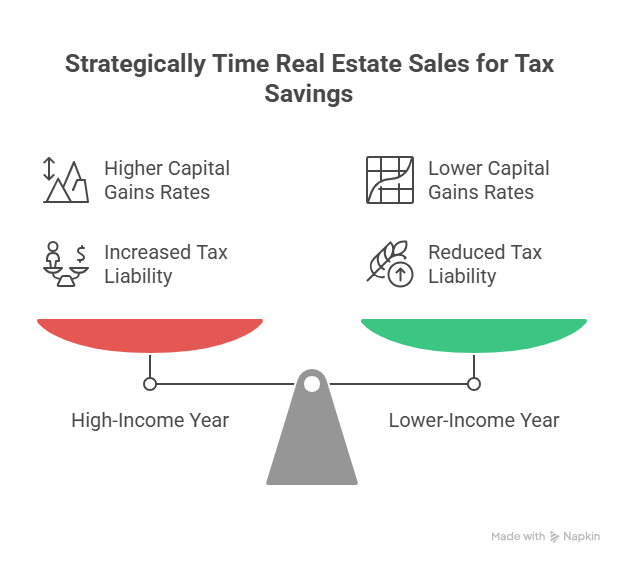

Strategic Timing Based on Income Levels

Capital gains rates are tied to your taxable income. Selling during a high-income year may push you into a higher capital gains bracket.

You may benefit from:

- Selling during a lower-income year.

- Offsetting gains with harvested losses.

- Coordinating the sale with retirement or business transitions.

Short-term capital gains (assets held under one year) are taxed at ordinary income rates. Simply holding beyond the one-year mark may reduce your rate considerably.

This type of income modeling makes a substantial difference in your total liability when evaluating how to avoid capital gains tax on real estate effectively.

Installment Sales Can Spread the Tax Burden

An installment sale allows you to obtain payments over multiple years rather than all at once. You recognize gains proportionally as payments are received.

This strategy may:

- Keep you in a lower tax bracket.

- Improve cash flow predictability.

- Reduce immediate tax exposure.

However, interest income must be reported separately, and default risk should be evaluated carefully.

Installment planning is frequently ignored but can be powerful in the right scenario.

Converting Rental Property to a Primary Residence

Another advanced strategy involves converting a rental property into your primary residence before selling.

While the Section 121 exclusion may apply, it is subject to:

- Non-qualified use allocation.

- Depreciation recapture.

- Ownership timeline rules.

The portion of gain attributable to rental years after 2008 generally cannot be excluded.

This means timing and allocation calculations matter significantly. The IRS formula is precise, and errors can be costly.

Offset Gains With Capital Loss Harvesting

If you have investment losses in stocks, mutual funds, or other capital assets, you may offset real estate gains.

Net capital losses:

- Offset capital gains dollar-for-dollar.

- Offset up to $3,000 of ordinary income annually if excess losses remain.

Coordinating portfolio losses with real estate sales requires planning before year-end.

We incorporate this analysis into broader real estate tax planning strategies when reviewing upcoming property sales.

Real Estate Tax Deferral Through Opportunity Zones

Opportunity Zone investments allow deferral of capital gains when reinvested into Qualified Opportunity Funds within 180 days of the sale.

While the deferral period has limitations based on current law, potential benefits include:

- Deferral of original gain.

- Potential basis step-up.

- Exclusion of appreciation on the Opportunity Zone investment if held long enough.

This strategy carries higher investment risk and requires careful due diligence. It is not suitable for every investor, but it can be powerful when aligned with your portfolio goals.

Planning Early Strengthens Your Position

Most tax-saving opportunities disappear once the sale closes.

Before listing your property, consider:

- Reviewing adjusted basis.

- Calculating estimated gain.

- Evaluating depreciation recapture.

- Exploring reinvestment timelines.

- Modeling different sales years.

If you are actively researching how to avoid capital gains tax on real estate, the best time to plan is before contracts are signed, not during tax season.

Skyline Financial CPA Houston regularly integrates these projections into comprehensive real estate tax consultations, so you understand your full exposure in advance.

In Closing

Understanding how to avoid capital gains tax on real estate requires more than reading general advice. Your income level, property type, depreciation history, and future goals all shape the optimal strategy.

If you are considering selling property this year or next, schedule a consultation with Zahra today. Proactive planning with her help can preserve more of your equity and reduce unexpected tax surprises.

FAQs

- Can you defer capital gains tax indefinitely with a 1031 exchange?

Yes, you may continue deferring gains by repeatedly exchanging into new properties. However, depreciation recapture and estate considerations should still be reviewed.

- What is real estate tax deferral, and how does it work?

Real estate tax deferral allows you to postpone paying capital gains tax by reinvesting proceeds into qualifying assets, such as like-kind property or Opportunity Zone funds.

- Do I pay capital gains if I reinvest in another property without a 1031 exchange?

Yes. Without properly structuring a 1031 exchange, reinvesting alone does not defer the gain.

- How does depreciation affect my capital gains calculation?

Depreciation reduces your property’s adjusted basis, increasing taxable gain. The amount claimed is typically recaptured at a maximum 25% rate.

- Is holding property longer always better for tax purposes?

Not necessarily. While long-term capital gains rates are lower than short-term rates, income timing, basis adjustments, and strategic reinvestment may matter more than a simple holding period.