When you own rental properties, your numbers tell the reality of performance. Property management accounting is not just about tracking rent deposits and expenses. It is about giving you clarity, protecting your cash flow, and helping you make informed financial decisions.

If your books are disorganized or reactive, your profits and tax position can quietly suffer. With the right CPA strategies, you can shift from simply recording transactions to building a financial structure that supports long-term stability and growth.

Below, you will find practical, Houston CPA-level insights by Zahra Samji to strengthen your reporting, improve visibility, and protect your income.

Why Having Clean Books is More Important Than High Rental Income

High rental income does not automatically mean strong financial health. If your accounting lacks structure, you may:

- Overestimate available cash.

- Miss legitimate deductions.

- Underfund repair reserves.

- Create compliance risks.

You should be able to see exactly how each property performs. When financial records are accurate and categorized properly, you gain confidence in your numbers. Instead of reacting to surprises, you make decisions based on reliable data.

If your reporting lacks structure, professional accounting services Houston can help you build a system tailored to your rental operations rather than relying on generic bookkeeping templates.

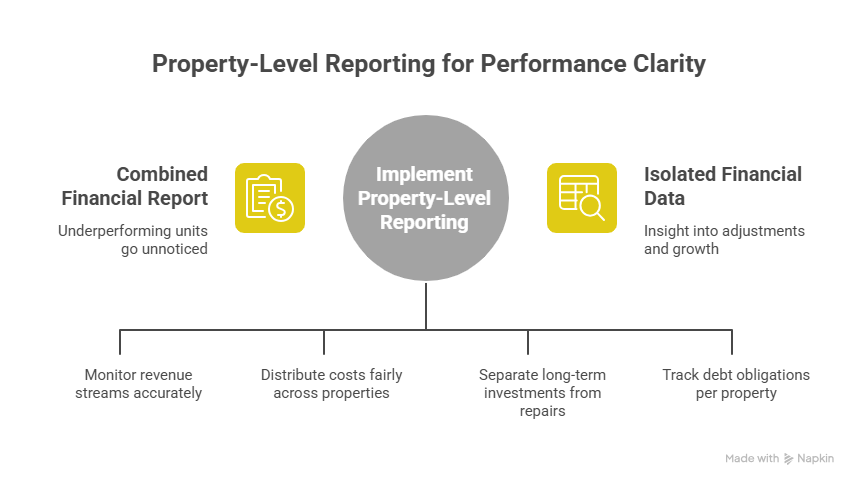

Separating Property-Level Reporting for Performance Clarity

One overlooked strategy in real estate accounting is separating activity by property instead of combining everything into one general report.

Your accounting system should allow you to:

- Track income by property and by unit when necessary.

- Allocate shared expenses accurately.

- Distinguish capital improvements from routine repairs.

- Monitor loan balances by property.

Without property-level tracking, underperforming units may go unnoticed. When you isolate financial data, you get insight into where adjustments are needed and where growth opportunities exist.

Property Management Accounting and Cash Flow Timing Gaps

Cash flow problems often come from timing differences rather than a lack of profitability.

For example:

| Situation | Accounting Effect | Cash Flow Effect |

| Late rent payment | Revenue delayed | Mortgage still due |

| Major repair invoice | Expense recorded immediately | Cash balance reduced |

| Security deposit received | Liability recorded | Not available for spending |

You should monitor both profitability and liquidity. Many landlords focus only on profit and loss statements. However, your cash position determines whether you can comfortably manage unexpected expenses.

Projecting at least three months ahead allows you to prepare for insurance renewals, tax payments, or seasonal vacancies before they impact your reserves.

Proper Handling of Security Deposits

Security deposits are liabilities, not income. Recording them incorrectly inflates revenue and distorts financial reporting.

You should:

- Record deposits in a liability account.

- Track balances by tenant.

- Keep them separate from operating funds when required.

Clear tracking protects you legally and ensures your financial reports reflect true operating income instead of overstated figures.

Correct Classification of Repairs and Capital Improvements

Misclassification of expenses is a common issue in rental property bookkeeping and can create headaches in property management accounting.

Repairs are routine costs that maintain property condition, such as fixing plumbing leaks or replacing minor components. These are generally deductible in the year incurred.

Capital improvements extend the life or increase the value of the property, such as roof replacements or major renovations. These costs are depreciated over time.

If you classify these incorrectly, you may either overstate deductions or miss tax-saving opportunities. Accurate classification protects both your compliance position and your long-term planning.

Building Strategic Reserves for Stability

Many landlords set aside funds casually without a structured plan. Instead, you should establish defined reserves:

- Operating reserves covering three to six months of expenses.

- Capital reserves for long-term improvements.

- Vacancy reserves for turnover periods.

Without intentional planning, temporary disruptions may force you to rely on credit. Structured reserves protect your cash flow and give you flexibility during slower periods.

Avoiding Commingling of Funds

Mixing personal and rental funds creates more than bookkeeping confusion. It increases audit risk, weakens liability protection, and complicates financing applications.

You should set up separate bank accounts and credit cards for rental operations. Clear separation simplifies year-end tax preparation and strengthens your documentation for property management accounting if questions arise.

Strategic Depreciation Planning for Long-Term Results

Depreciation is not just an annual calculation. When planned strategically, it can significantly affect both current taxes and future exit strategies.

You should evaluate:

- Cost segregation opportunities.

- Partial asset dispositions during renovations.

- Bonus depreciation eligibility.

- Long-term impact on capital gains.

Proper planning ensures you benefit from available deductions while understanding the future tax implications of selling or refinancing.

Establishing a Disciplined Monthly Close Process

A structured monthly review prevents small errors from becoming major issues.

Your monthly process should include:

- Reconciling bank and credit card accounts.

- Matching rent rolls to deposits.

- Reviewing outstanding invoices.

- Updating loan balances.

- Comparing performance to prior months.

This discipline gives you clarity. Instead of waiting until tax season, you maintain continuous control over your financial position.

Forecasting Future Growth With Reliable Financial Data

When your records are accurate, forecasting becomes meaningful. You can evaluate:

- The impact of vacancy increases.

- Whether you can support new acquisitions.

- How rising expenses affect margins.

Reliable reporting allows you to expand strategically rather than reactively. Growth decisions should be based on data, not assumptions.

Conclusion

Strong financial management is not accidental. When your accounting structure is organized, compliant, and strategically designed, your properties generate predictable results. Property management accounting supports clearer decision-making, stronger liquidity, and long-term portfolio growth.

If you want accurate books, improved cash flow visibility, and guidance tailored to your rental operations, CPA Houston Zahra can help you build a financial framework that supports sustainable growth. Schedule a consultation today and take control of your numbers with clarity.

Property Management Accounting FAQs

- How often should I review rental property financial reports?

You should review them monthly. Consistent oversight helps you catch discrepancies early and maintain strong cash flow management.

- Should I use cash or accrual accounting for rental properties?

Cash basis is common for small portfolios, but accrual accounting provides a more accurate performance picture for multiple properties.

- Can poor bookkeeping affect refinancing opportunities?

Yes. Lenders require accurate financial reports. Disorganized records may delay or complicate loan approvals.

- What is the most common accounting mistake landlords make?

Combining personal and rental funds is one of the most frequent and costly errors.

- When should I consult a CPA for rental properties?

If you own multiple properties, are expanding, restructuring entities, or dealing with IRS issues, professional guidance can prevent costly mistakes.